The Full Story:

The art of successful investing requires constantly adjusting frameworks, biases, and scopes. Construct a faulty framework and returns will faulter. Adhere to faulty biases and markets will humiliate you. Focus off-target and you will miss by a mile. Often, market activities have obvious origins. A global pandemic that threatens our lives and livelihoods to a significant but unknown degree should trigger a historic selloff, and it did. But, with equal frequency, market activities have unobvious origins. Amidst dramatic civil unrest and a resurgence in COVID cases this week, the NASDAQ hit an all-time high. How can two similar environments create such dramatically different results? Because COVID powered the first reaction while M2 powered the second.

A Fed Chairman’s Biggest Fear

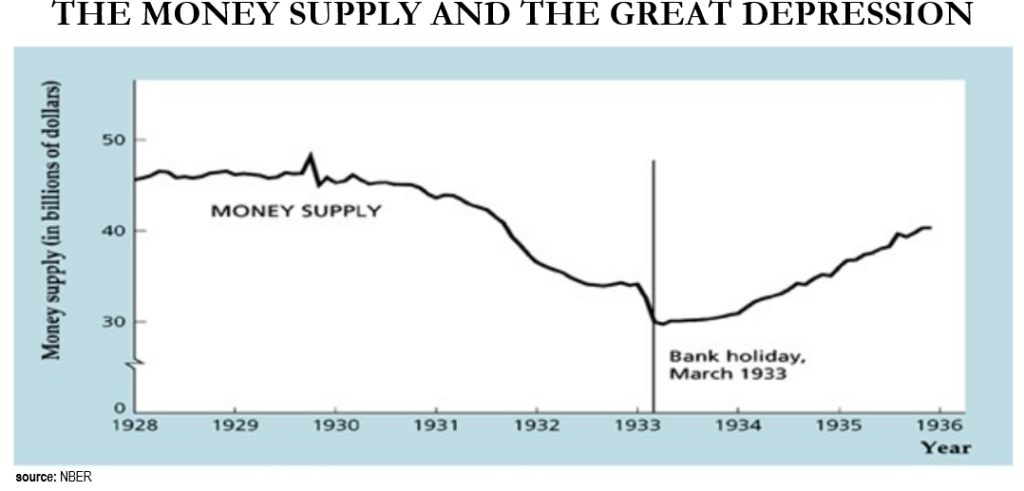

This week, Fed Chairman Jerome Powell reiterated the Fed’s commitment to anchoring rates near zero while supplying infinite quantitative easing. For those of you who haven’t read Milton Freidman and Anna J Schwartz’s classic “A Monetary History of the United States” written in 1963, allow me to introduce to you the algorithm behind all modern central bank policy decisions: MV=PQ. M = Money Supply (also known as M2), V = Money Velocity, P = General Price Levels, and Q = Economic Output. In short, the amount of money in circulation (M), and the speed by which it circulates (V), determines total inflation-adjusted GDP (PQ). Velocity represents the trickiest component within the equation. Simplistically, when economic actors feel confident, velocity rises and when economic actors feel hesitant, velocity falls. While marketplace sentiment controls velocity, the Fed controls the money supply. In “A Monetary History of the United States”, Milton and Anna closely examined the relationship between money supply and economic output during the country’s most extreme economic event – the Great Depression:

During the Great Depression, monetary velocity crashed as banks failed and consumers withdrew. Concurrently, the money supply evaporated, COMPOUNDING the hit to GDP (smaller M* smaller V = smaller GDP). Given the Fed’s ability to control the supply of money, the failure to offset falling velocity (V) with rising money supply (M) effectively proved that inaction by the Fed turned a deep recession into The Great Depression. In the words of ex-Fed Chairman Ben Bernanke reflecting upon Milton and Anna’s work, “Let me end my talk by abusing slightly my status as an official representative of the Federal Reserve. I would like to say to Milton and Anna: Regarding the Great Depression, you’re right. We did it. We’re very sorry. But thanks to you, we won’t do it again.”

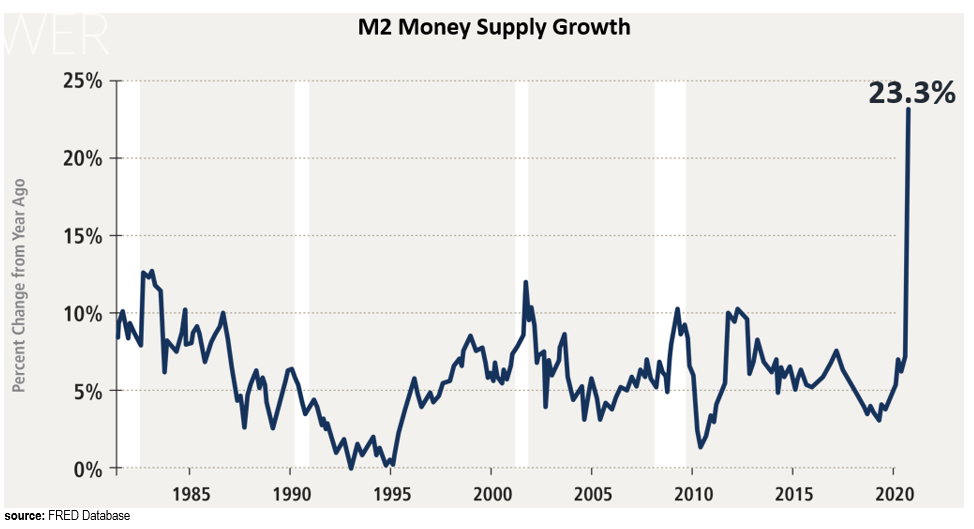

Few events can cause the collapse in velocity (global quarantines) on the scale of a pandemic. In response, Fed Chairman Jerome Powell has increased the money supply at an astounding and historic rate:

Just this week, Chairman Powell signaled his willingness to increase this breakneck pace of money creation even further. Essentially asserting that he will not incite The Great Depression 2.0. But what happens if velocity rises rapidly while money supply rises rapidly? If a collapse in velocity and a collapse in money supply created the Great Depression, then a rapid expansion in velocity and a rapid expansion in the money supply could create the Great Expansion! Here are three charts that demonstrate the amount of latent economic accelerant awaiting a turn in velocity:

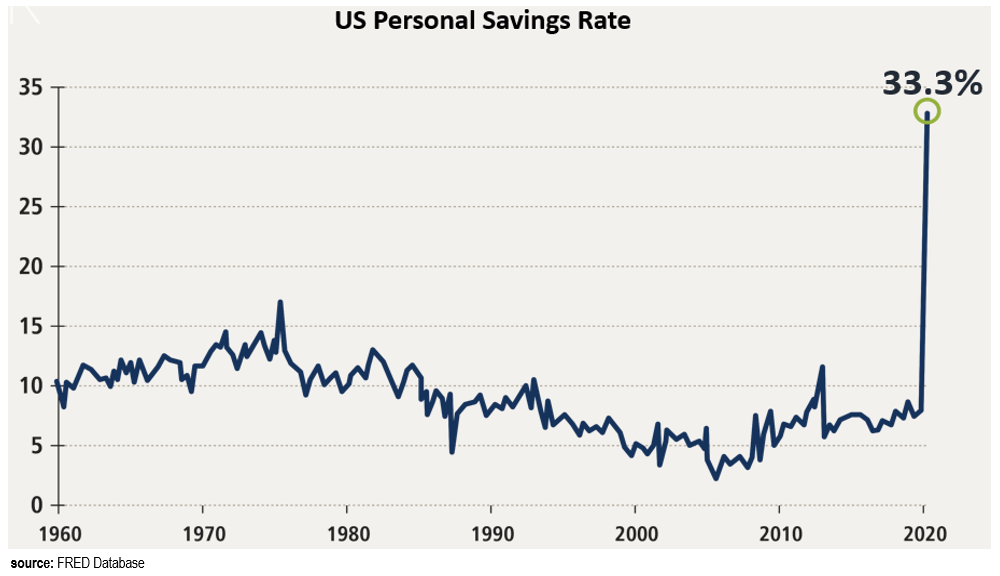

Consumer Accelerant:

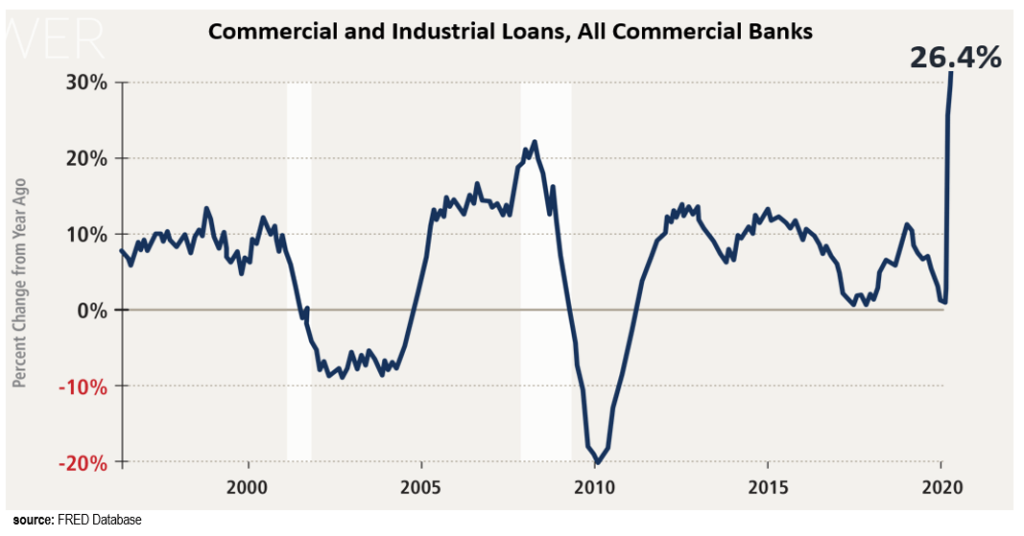

Corporate Accelerant:

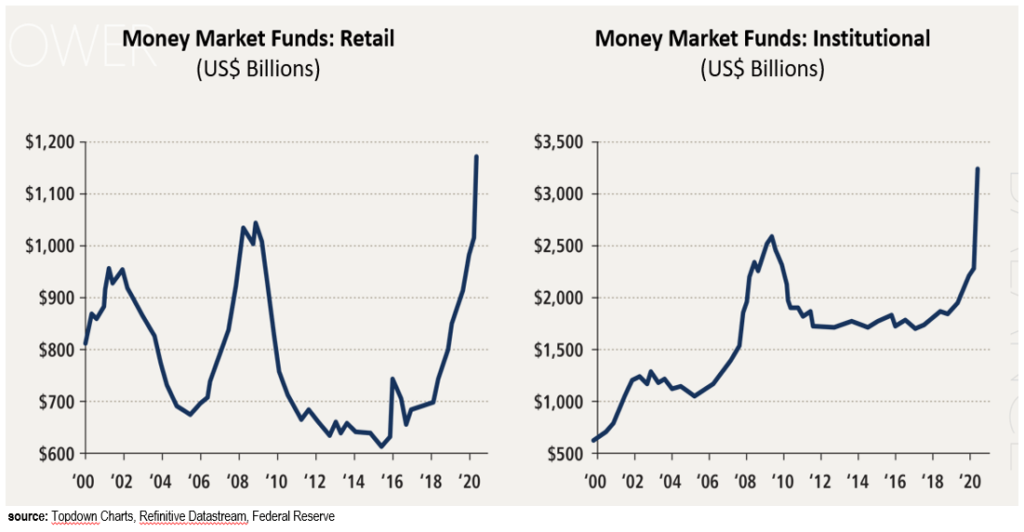

Investor Accelerant:

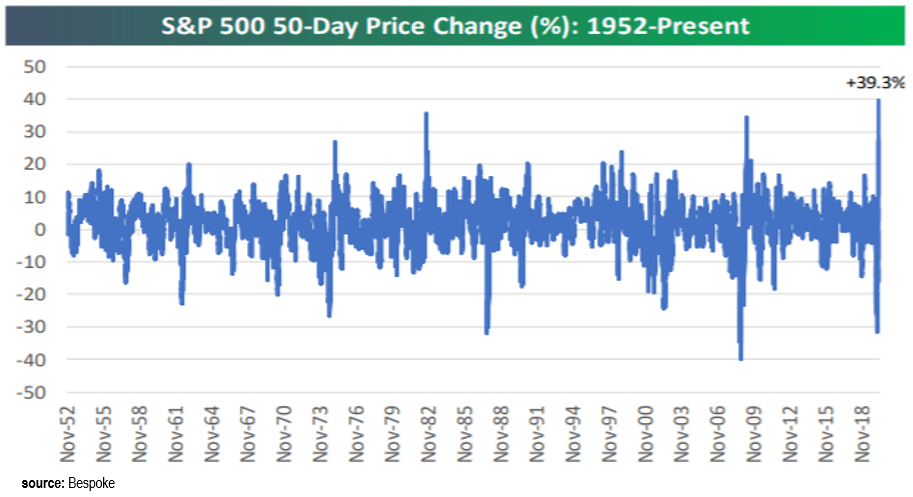

Jerome Powell has flooded this economy with cash and its accumulating EVERYWHERE. While it may not have started sloshing down Main Street due to contagion fears and lockdown restrictions, it surely will. It has definitely been sloshing down Wall Street, which lacks COVID restrictions. In fact, over the last 50 days, the stock market has posted its largest gain ever:

In short, the historic increase in money supply has already resulted in historic gains on Wall Street. As restrictions abate and velocity rises, we could see historic gains for Main Street as well.