On Iran

Iran was established as a religious state in 1979 when the Ayatollah Khomeini overthrew the incumbent monarchy and became the Supreme Leader. Over the last 40 years, the iron fist of Islamic leadership has suppressed efforts of the Iranians to establish a durable market-based economy…a path Iran was on prior to insurrection. The new Islamic regime nationalized industry and established a central economic governance system consisting of 5-year master plans with subsidies and price controls. As a result, international capital fled Iran, private sector development collapsed, and GDP growth became wholly dependent on state-owned oil production.

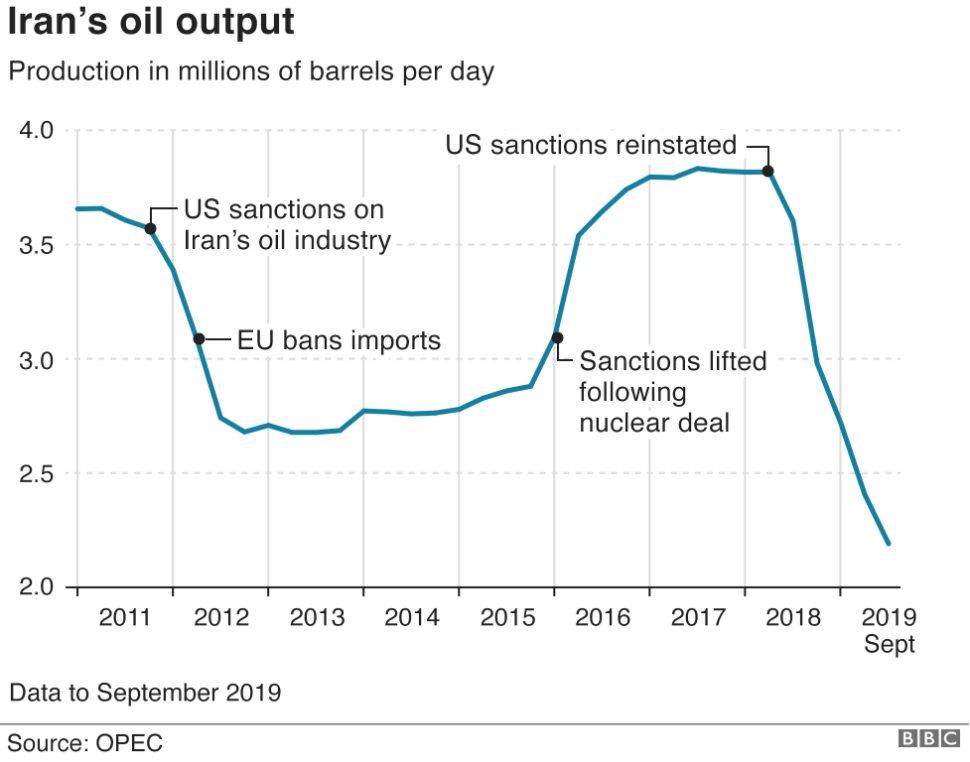

At its recent peak, Iran produced nearly 4 million barrels of oil per day, servicing about 4% of global demand (Iran itself consumes 2 million barrels per day). Following the Trump sanctions imposed in early 2018, oil production in Iran has plummeted to just over 2 million barrels per day with exports falling below 200,000 barrels per day. In comparison, the US now produces nearly 13 million barrels of oil per day and has essentially weaned itself off of imported oil. As a key takeaway, the global economy has clearly proven its ability to function without Iranian oil.

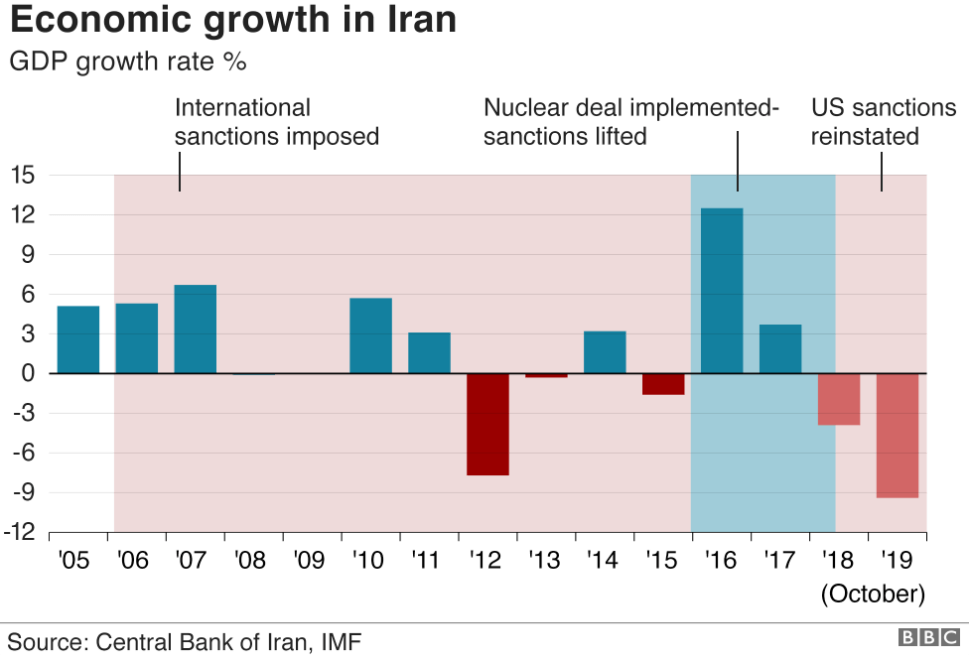

With a GDP of roughly $450 billion, the size of the Iranian economy approximates that of Maryland…and it is shrinking. The IMF estimates that Iran’s GDP shrank 4.8% in 2018 and another 9.5% in 2019 with no growth expected in 2020. Its population of 80 million operates at a per capita GDP level below $6,000 with an unemployment rate of 20%. The national currency, the Iranian dinar, has recently lost 50% in value, causing consumer inflation rates to top 30% over the last 2 years. As a result, thanks to a baby boom in the early 2000s, Iran’s population consists mostly of hungry, angry, well-educated young people without any economic prospects. Predictably, violent protests have erupted. Towards the end of 2019, 1500 protesters were reportedly killed across Iran as the government cracked down forcefully on dissent. To limit subsequent hysteria and coordinated counterattacks, the Iranian government unplugged the internet for a week, adding further injury to its economy and public standing. As a key takeaway, even with the Iranian economy in shambles, the global economy continues to grow.

Given the internal instability facing the Iranian regime, the threat of external instability in the wake of Soleimani’s execution couldn’t come at a worse time. Simultaneously angering America, its neighboring allies, and its own citizenry could quickly lead to regime change. Those in power often prefer to stay in power and for this reason, we believe the market has correctly predicted that Iran will fold. Trump has even opened the door to renegotiations. Reason would suggest that this might be the preferred path to revive the Iranian economy and reduce internal pressures, rather than inviting further sanctions with bloodshed. Regardless of the path chosen, a complete departure of Iran from the global economy and oil markets would still not systematically destabilize the global economy. Losing Maryland would matter more.